Life insurance is an important financial tool for United States citizens, providing financial protection and peace of mind for their families and loved ones. Here’s a comprehensive overview of life insurance in the U.S.

Types of Life Insurance:

- Term Life Insurance:

- Coverage: Provides coverage for a specific period, such as 10, 20, or 30 years.

- Benefits: Generally lower premiums compared to permanent insurance. Pays a death benefit if you pass away during the term.

- Limitations: Coverage ends when the term expires, and there is no cash value component.

- Whole Life Insurance:

- Coverage: Provides lifelong coverage with guaranteed death benefits.

- Benefits: Includes a savings component known as cash value that grows over time and can be borrowed against or used to pay premiums.

- Limitations: Higher premiums compared to term life insurance.

- Universal Life Insurance:

- Coverage: Offers flexible premium payments and adjustable death benefits.

- Benefits: Includes a cash value component that earns interest. Policyholders can adjust the death benefit and premium payments within certain limits.

- Limitations: Complex and can be expensive if not managed properly.

- Variable Life Insurance:

- Coverage: Provides flexible premiums and death benefits with a cash value component that can be invested in various accounts.

- Benefits: Potential for higher returns on cash value through investment options.

- Limitations: Investment risks are associated with the cash value component, which can affect the policy’s performance.

- Final Expense Insurance:

- Coverage: Designed to cover funeral and burial expenses.

- Benefits: Generally easier to qualify for, with smaller coverage amounts.

- Limitations: Limited coverage amount compared to other types of life insurance.

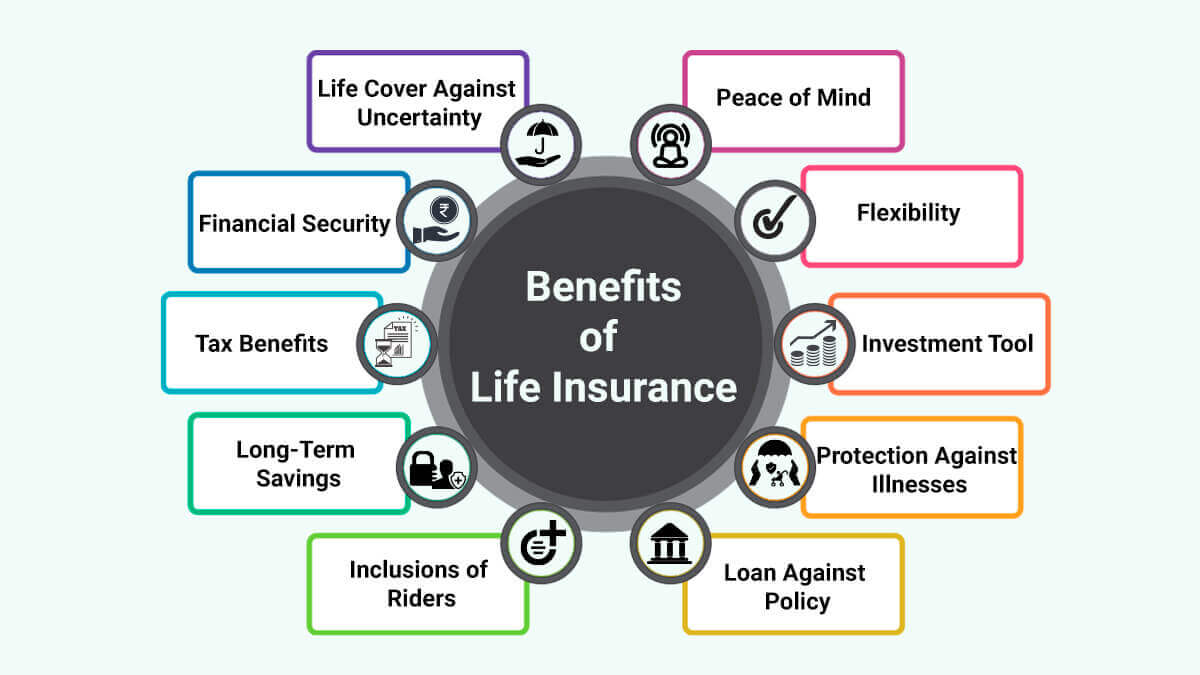

Key Benefits of Life Insurance:

- Financial Protection for Loved Ones:

- Provides a death benefit to beneficiaries, helping cover living expenses, debt repayment, and other financial needs.

- Income Replacement:

- Replaces lost income if the policyholder passes away, ensuring that dependents can maintain their standard of living.

- Debt Coverage:

- Helps pay off outstanding debts, such as mortgages, loans, and credit card balances, reducing financial burden on survivors.

- Estate Planning:

- Assists in managing estate taxes and other expenses, ensuring that more of the estate goes to heirs.

- Cash Value Accumulation:

- Permanent life insurance policies accumulate cash value over time, which can be borrowed against or used to pay premiums.

- Business Continuity:

- Can be used in business planning, such as funding buy-sell agreements or covering key person insurance needs.

- Peace of Mind:

- Provides peace of mind knowing that loved ones will be financially protected in the event of the policyholder’s death.

Choosing the Right Policy:

- Assess Your Needs:

- Determine how much coverage you need based on factors like income, debts, and future financial needs of your dependents.

- Consider Policy Types:

- Choose between term, whole, universal, or variable life insurance based on your financial goals, budget, and preferences.

- Compare Quotes:

- Obtain quotes from multiple insurers to compare premiums, coverage options, and policy features.

- Review Financial Strength:

- Check the financial stability of the insurance company to ensure they can meet their obligations.

- Understand Policy Terms:

- Read and understand the policy terms, including any exclusions, limitations, and benefits.

- Consult a Financial Advisor:

- Consider consulting a financial advisor or insurance agent to help navigate your options and choose the best policy for your situation.

Life Insurance For United States Citizens:

Life insurance for non-U.S. citizens can be a bit more complex than for U.S. citizens due to various legal and logistical factors. However, many insurance companies in the U.S. do offer life insurance products to non-U.S. citizens. Here’s a guide to understanding life insurance for non-U.S. citizens:

Key Considerations:

- Residency Status:

- Permanent Residents: Non-U.S. citizens with permanent residency (green card holders) typically have access to the same life insurance options as U.S. citizens.

- Non-Residents: Non-U.S. citizens who are not permanent residents may face more limitations. Some insurers might offer coverage, but it often depends on the specific circumstances and the insurer’s policies.

- Coverage Types:

- Term Life Insurance: Available for both residents and non-residents, offering coverage for a specific period with generally lower premiums.

- Whole Life Insurance: Offers lifelong coverage with a cash value component, but may be more challenging to obtain for non-residents.

- Universal Life Insurance: Provides flexible premiums and adjustable benefits, but availability may vary based on residency status.

- Final Expense Insurance: Designed to cover end-of-life expenses, often available for non-residents but with potentially different terms.

- Application Process:

- Medical Underwriting: Non-U.S. citizens may be required to undergo additional medical underwriting or provide more detailed health information.

- Proof of Residency: Insurers might need proof of residency status, such as a visa, green card, or other documentation.

- Travel and Residency Restrictions: Some policies may have restrictions on travel or residency outside the U.S. or may not cover deaths that occur abroad.

- Premiums and Coverage Limits:

- Higher Premiums: Non-U.S. citizens might face higher premiums due to perceived higher risk or administrative complexities.

- Coverage Limits: The amount of coverage available might be limited, and certain types of coverage might not be offered to non-residents.

- Policy Exclusions:

- Exclusions for Non-Residents: Policies might have specific exclusions related to travel or residency, so it’s essential to understand these terms clearly.

Major Insurers Offering Life Insurance to Non-U.S. Citizens:

- MetLife

- Known for offering various life insurance products and may provide options for non-U.S. citizens, depending on residency status.

- Prudential Financial

- Offers a range of life insurance products and has experience working with international clients.

- New York Life Insurance

- Provides multiple life insurance options and may have products available for non-U.S. citizens with specific residency status.

- State Farm

- Offers term and permanent life insurance and may provide coverage to non-U.S. citizens with proper documentation.

- Northwestern Mutual

- Known for its comprehensive life insurance offerings, which may be available to non-U.S. citizens under certain conditions.

- Guardian Life

- Provides various life insurance products and might offer options for non-U.S. citizens based on their specific needs.

Steps to Obtain Life Insurance:

- Determine Eligibility:

- Verify your eligibility with insurers based on your residency status and any specific requirements.

- Compare Quotes:

- Obtain and compare quotes from multiple insurers to find the best coverage and rates for your situation.

- Understand Policy Terms:

- Review policy terms carefully, including any exclusions or limitations related to residency or travel.

- Consult with an Agent:

- Work with an insurance agent or broker who has experience with international clients to help navigate the application process and find suitable coverage.

- Provide Necessary Documentation:

- Be prepared to provide proof of residency, visa status, and any other documentation required by the insurer.

Life insurance for non-U.S. citizens involves additional considerations, but with the right approach and guidance, it is possible to find suitable coverage.

Major Life Insurance Companies in the U.S.:

- Northwestern Mutual

- New York Life Insurance

- Prudential Financial

- MetLife

- State Farm

- MassMutual

- John Hancock

- Nationwide

- Lincoln Financial Group

- Guardian Life

Each company offers a variety of life insurance products with different features and benefits. It’s important to evaluate your individual needs and circumstances to select the most suitable policy.